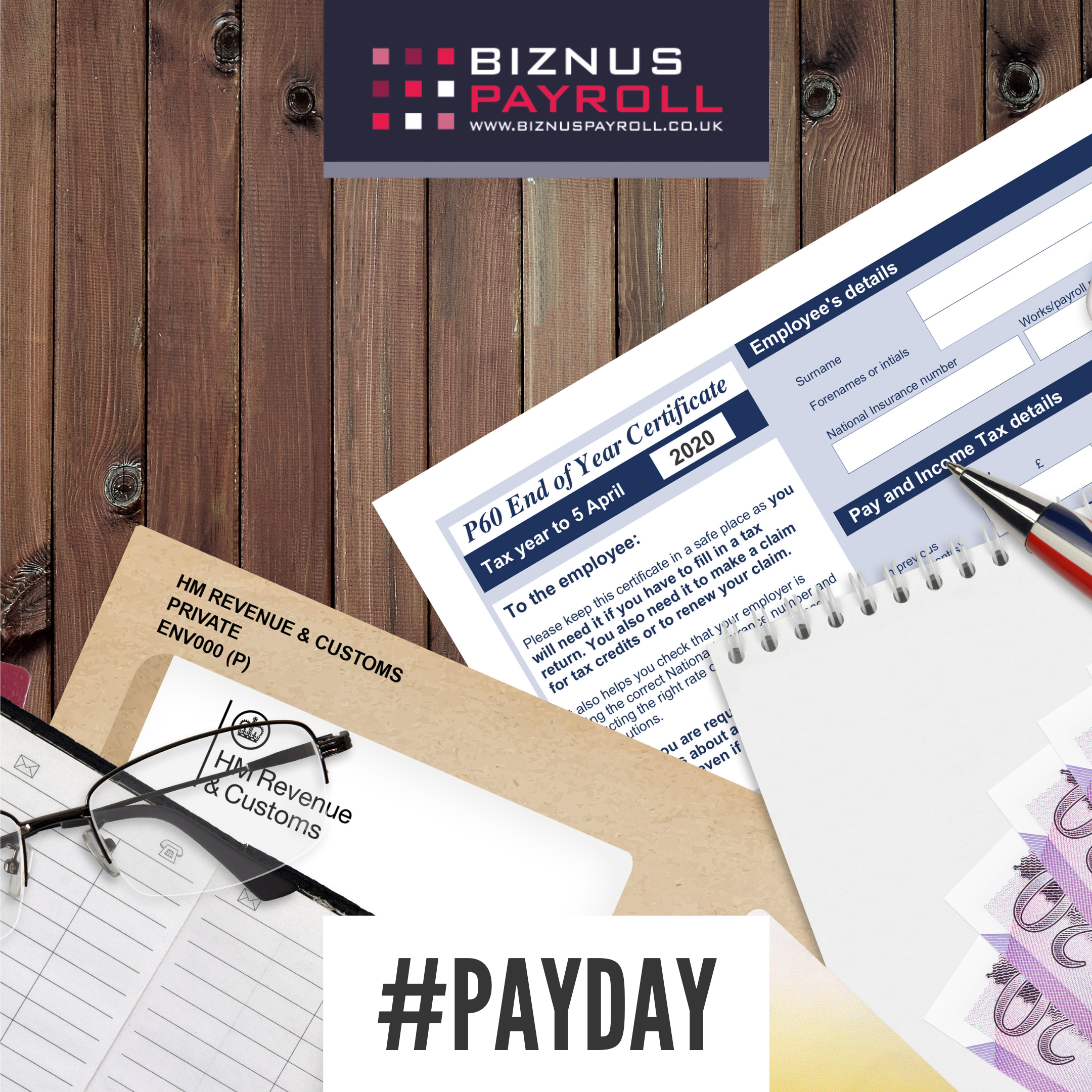

What is a P60?

What is a P60?

A P60 is a certificate that summarises an employee’s total pay and deductions for the tax year just ended. It gives details of their pay, pension and or working tax credits received. It shows income tax and national insurance contributions (NIC) paid; student and or postgraduate loan repayments; and statutory payments, such as maternity and paternity pay. It also gives a final tax code. Employees get a separate P60 for each job they have.

Who gets a P60 and why?

Each year, you must give the P60 to every employee who was paid in the tax year and still working for you on 5 April – the last day of the tax year; and for anyone, you have completed a P11 deductions working sheet or submitted on an RTI full payment submission (FPS). Limited company directors who take a salary, also require a P60. Sole traders do not draw a salary, so do not need to issue themselves a P60, but they must give one to any active employee. Workers that left employment and were issued a P45 before the 5 April do not require a P60.

How long should an employer keep them?

The law requires employees to keep a record of their taxable income for at least 22 months after the end of each tax year. However, Biznus Payroll Ltd advises that they keep their P60 safe for life. They may need it to prove how much tax and NI they have paid in years to come – for example, as proof of NI contributions for a state pension, to complete a tax return; claim back overpaid tax; or apply for anything means-tested such as tax credits. Employees may also need it as proof of income, for example, if they apply for a loan or mortgage.

As outlined by HMRC, your employer must retain records of your P60 for three years, and should you need a copy at any point, they must provide you with one. Anything longer than three years, it is unlikely they will have any records and so it is vital that you retain each P60 every year.

When should they be issued by?

The P60 must be given to your employee by 31 May after the end of the tax year (5 April), so that, if you need to, you can complete a tax return or claim a repayment of tax. The only circumstance where an employer is not required to issue you with a P60 is if you have left their employment during the tax year.